Weekend Digest #333: Warsh, Interest Rates, Gold & Silver

Making sense of last week's volatility.

Summary

Kevin Warsh’s nomination as Fed Chair signals a shift toward tighter monetary policy, potentially ending the party for the “debasement trade”.

Warsh should deliver a couple of rate cuts in 2026, but will likely revert to a hawkish stance by year-end.

Markets had priced in aggressive stimulus; Warsh’s credibility as a policy hawk curbs runaway inflation expectations and puts downward pressure on long-term rates.

Gold remains a solid hedge, but silver and other industrial metals turned into a meme trade and have probably topped for now.

Author’s note: There’s too much going on to fit everything in a normal-sized Weekend Digest today. And the last time I tried to send out a 9,000-word article, Substack couldn’t deliver it to many people’s inboxes. So, we’re going with a two-parter this week to keep things manageable. First up, on Warsh, market reaction, gold and silver, etc. And then we’ll get to developments in LatAm and our portfolio holdings in Tuesday’s Part 2.

--

On Thursday, we learned that President Trump would nominate Kevin Warsh as the new Fed Chair to replace Jerome Powell. Warsh still has to be confirmed to make it official, but he’s qualified for the position and previously served on the Fed’s Board of Governors. So, he’s likely to be confirmed without much pushback.

Judging by the 30% drop in the price of silver on Friday, the market may have been a bit surprised by the news.

As I tweeted on Thursday night, prior to gold and silver plunging, this appears to be a potential regime change in terms of how people think about monetary policy, the dollar, and the so-called the debasement trade.

Over the ensuing days, I’ve seen a lot of confusion and misunderstanding on social media. And it’s worth elaborating on my original tweet, as there are some fair counterarguments to my view.

So, what happened, and why in particular was the Warsh pick such a big deal for currencies, precious metals, and crypto?

--

The most common complaint I saw was that metals and crypto shouldn’t have gone down... it’s not like Warsh is going to raise interest rates or anything, so what’s the matter?

And indeed, he’s not going to raise rates. Rather, he will cut rates.

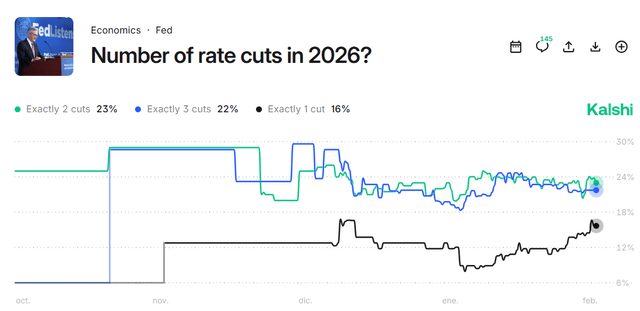

In fact, rate cut betting odds for 2026 barely moved once the Warsh pick was announced.

The odds of exactly one rate cut in ‘26 have crept up slightly over the past couple of weeks, but the market continues to price pretty solid odds of either two or three rate cuts this year, and the Warsh pick didn’t change the math there at all.

There are people posting stuff like the following, which is just not right -- there’s not going to be any rate hikes in the near future:

Plenty of prominent metals/crypto bulls are knocking down some variant of this straw man argument... of course there won’t be rate hikes. Thus, the sell-off Friday was unwarranted.

That’s not it though. No institutional money/fund managers think Warsh is going to hike interest rates in 2026.

There’s a more nuanced phenomenon occurring here.

--

Anyone that Trump picked to be the new Fed chair was going to cut interest rates in 2026. This wasn’t in doubt. Warsh knows his immediate assignment.

Rather, what’s interesting is what happens past the near-term event horizon. Warsh makes the first couple of rate cuts, and then it’s time to focus on long-term positioning. What happens at this juncture?

This gets to the question of whether he’s a changed man or whether he’s still instinctively a policy hawk.

Let’s back up.

For those that weren’t following markets back then, Warsh was a key figure during the 2008 Financial Crisis. He was on the Fed Board of Governors. And not only that, he served as the Fed Board’s key liaison to Wall Street, helping communicate policy and work out moves during the height of the financial crisis.

Simply put, despite his young age at the time, Warsh was a highly influential figure during the financial crisis. And, according to critics, he was far too preoccupied with inflation in 2008 and misjudged the risk/reward between fighting inflation and supporting the U.S. housing market/banking system.

Keep in mind that, like today, we had skyrocketing commodity prices in 2008. The dollar had been plunging for years at that point amid the U.S.’ failing Middle Eastern wars and sluggish economic performance at home. The Chinese commodity supercycle was in full swing, and emerging markets were soaring.

At the time, Warsh was looking at a price of oil that had soared to $147 per barrel (up from the double digits just months prior). Voters were furious about record high gasoline prices, and were set to vote in a young senator, Barack Obama, as U.S. President in order to punish the Bush Administration for the surge in gas prices combined with the poor labor market.

Actually, there does appear to be a fair resemblance to today, doesn’t there? President Trump’s approval rating has slumped over the past year, Democrats are heavy favorites to win the upcoming 2026 Congressional elections, and voters are furious about higher grocery prices and the bad labor market.

Thankfully, we don’t just have to theorize here.

We can see how Warsh reacted when facing 2008’s conditions where there was both:

1. Too much inflation, runaway commodity prices, and a tanking U.S. dollar.

2. A financial market bubble (then housing, now AI) papering over an otherwise crummy economy.

Here’s where things get rough for the pro-inflation side of the debate.

Let’s take some vintage Warsh quotes from 2008.

Here he is in March 2008, the exact month that Bear Stearns went bust. Did that color his view. Nope!

“On the inflation front, there is little reason to be confident that inflation will decline. There are reasons to believe that our inflation problems will become more pronounced and, I fear, more persistent.”

Fast forward to June 2008. Countrywide Financial and other subprime housing lenders have failed. S&P 500 earnings estimates are starting to tank. Is Warsh moderating his views? Decide for yourself:

“Inflation risks, in my view, continue to predominate as the greater risk to the economy.”

It’s now September 2008, a month in which the S&P 500 declined 20% peak-to-trough. We’re now just weeks ahead of the Lehman Brothers failure, AIG bailout, and all that. How is Warsh feeling in September?

“I’m still not ready to relinquish my concerns on the inflation front.”

And there you have it.

This guy, when faced with the worst U.S. economic crisis since the 1930s, was a fiscal hawk to the bitter end.

Actions matter more than words. Warsh said the right stuff to get Trump to nominate him, sure. But do we think a guy that was against stimulus/rate cuts/bailouts through the financial crisis is suddenly going to slash rates to zero just because Trump sends out some nasty tweets?

--

Now, to be fair, we’re more than 15 years removed from the end of the Financial Crisis era. Economists learned lessons from what happened, and some folks that were very Austrian/hard money/hawkish then have since softened their views. It’s possible Warsh would take a much different policy direction if faced with a similar crisis today.

And, if you do want to make the case that he’s changed, there is some evidence for that. Namely, in recent Warsh speeches, he’s gone on at length about how artificial intelligence and other tech advances are going to end up being significantly deflationary. Companies will use less human labor, and it’s much easier to substitute in robots/automation anytime humans go on strike, demand higher wages, or otherwise gum up the works. The infamous 1970s wage/price spiral and ensuing stagflation is far less likely to occur now given subsequent technological developments.

Warsh’s argumentation there is reasonable, in fact, I share that view. (While I’m skeptical of AI boosters’ promises today, there’s little doubt it will transform the economy over the next 10-20 years. Like with the internet bubble in the 1990s, dot-com investors were early, rather than entirely wrong...)

More broadly, I hold the (currently contrarian) view that developed market interest rates are going to back to zero over the next 5-10 years. And much of my thinking for that is based in a combination of demographics and technological advancements -- in other words, along the lines of Warsh’s argument.

--

However, I think it’s short-sighted to assume that because Warsh thinks AI is deflationary it means he’s going to suddenly turn into a policy dove that is going to slash interest rates directly to zero and drown the economy in freshly printed dollars.

The market was betting on Trump’s new hyper-dovish Fed chair giving us this. Turns out, Warsh is not going to give us this.

--

Let’s square the circle here.

Warsh will cut interest rates a couple of times once he takes over at the Fed. He probably wants to initially please Trump. There’s no way of knowing what was said when Trump and Warsh were meeting over the past year, but I’d assume Trump has confidence that Warsh will cut interest rates and toe the party line in 2026. Again, market odds on the number of rate cuts in 2026 didn’t change at all once Warsh was already announced; the cake was already baked.

However, the Federal Reserve remains an independent institution. There’s nothing Trump can do to force Warsh to keep cutting rates indefinitely.

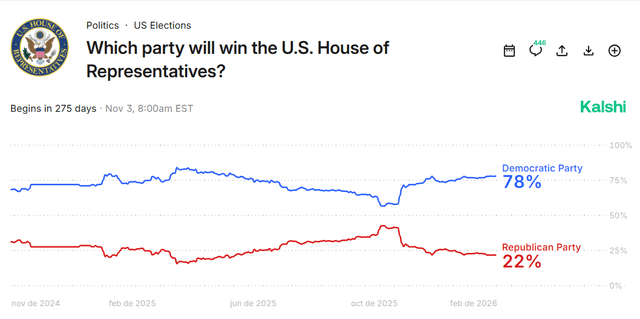

And, I’d guess, particularly once Midterm elections occur in November and the Democrats regain control of Congress, Warsh and the Fed Board will feel free to act as they wish regardless of Trump’s latest tweets.

On the upcoming midterms in particular, consider the following graph:

Note the decline in Republican odds since November 2025. We’ll come back to this in a minute when we get to the real reason why Trump picked Warsh.

--

In Kevin Warsh, we have someone who is hawkish in his blood and his conviction wasn’t shaken even during the 2008 Financial Crisis.

And, let’s cast some cold water on the idea that Warsh is a changed man following 2008. Did he regret his hawkish stance? Not at all. Here is Warsh in 2018, making remarks on lessons learned 10 years out from the crisis:

“My overriding concern about continued QE [quantitative easing], then and now, involves the misallocations of capital in the economy and the misallocation of responsibility in our government. Misallocations seldom operate under their own name. They choose other names to hide behind. They tend to linger for years in plain sight. Until they emerge with force at the most inauspicious of times and do unexpected harm to the economy.”

Does that sound like a man who was humbled by the 2008 bank failures and has now become a full-blown Keynesian stimulus dealer? Nope!

My argument is that Warsh is likely to be worried about “misallocations” of capital from speculative manias. I don’t think he’ll be running to the market’s rescue every time the S&P drops five or ten percent. I simply don’t believe we should discard a lifetime of one’s views and actions based simply on a couple of recent speeches, particularly when he was angling to obtain the Fed chair post and needed to soften his image to get Trump’s nod.

All this to say that there’s a good chance Warsh goes back to being a monetary hawk, or at least heads toward that direction once the midterm elections are over.

Keep in mind that Warsh’s term will run through 2030 -- he’ll carry over well into the next presidency. Be it a Republican or Democrat, Warsh will not be under direct influence from Trump for a fair chunk of his time at the Fed.

Markets (especially credit markets) are longer-term discounting mechanisms. A person buying a 10- or 30-year bond isn’t just betting on economic policy at the next Fed meeting. Rather, you need to have a view on how things are going to go in coming years and even the next decade out.

Having someone who was fervently opposed to stimulus in the 2008 Financial Crisis is a major tonal shift.

Be it because of AI disruption, the poor state of the economy now, or simply needing to promise Trump a couple of cuts to get the job, Warsh will do the president’s bidding for 2026. But there’s little guarantee he will be a dove beyond that.

And given that markets were already all-in on the “run it hot” “crash the dollar” etc. trade themes, any semblance of the opposite policy agenda should send a chill through risk assets.

--

But Ian, Trump wants massive rate cuts. Why is he picking a hawk to run the Fed?

Good question.

Let’s suppose Trump picked an uber-dove that was promising to slash interest rates to zero and do whatever the president wished. Or even better, let’s just say Trump was the Fed chair himself and he set the Fed benchmark interest rate to zero tomorrow.

S&P goes to 10,000, gold to 10,000, median house price to a million, Bitcoin also to a million, and Kimberly-Clark goes out of business because we start using dollar bills to wipe our backsides, right?

Probably not, actually.

But why not?

In the real world, if you overly stimulate the economy, creditors get irritated and stop lending money at low interest rates. In short, if the government starts acting irresponsibly, interest rates tend to go up. Countries that run ridiculous policies like Turkey, Zimbabwe, and Argentina (until recently) are economic laughingstocks. If unserious monetary policy were the path to success, more countries would be doing it.

The Fed (or any Central Bank) can set their overnight rate to whatever they want. But they don’t and can’t set longer-term interest rates. The market collectively does that. A combination of hedge funds, insurance companies, sovereign wealth funds, pensions, etc. are the marginal buyers (or sellers) of bonds. And if a government starts acting recklessly (say, running a 10% of GDP deficit), those folks start to dump their bonds until the government cuts out the bad behavior.

Usually, the so-called “bond vigilantes” strike because of excessive government spending. But, unwanted Central Bank tinkering/stimulus can also trigger a bond panic. Anything that causes people to worry that money will be devalued/inflation will spike is going to cause a sharp rise in longer-term interest rates.

I want to emphasize again that there is nothing that guarantees that short- and long-term interest rates have to go in the same direction at the same time.

Long-term interest rates go down when there isn’t much demand in the economy. This is usually a result of bad macroeconomic conditions (i.e. a recession) though sometimes other factors like demographics (see: Japan, last 30 years) also weigh in.

Setting interest rates to zero at a time when companies are spending a seemingly unlimited amount of money on AI gizmos is simply going to cause even wilder spending on said AI gizmos, creating a bigger economic downturn once the AI gizmo bubble pops.

Warsh gets this -- see his quote on how prior Fed QE simply created more misallocation of resources.

--

By contrast, and here’s where things get fun and counterintuitive, if you actually want lower long-term interest rates, you need to have tight monetary policy upfront.

Stop and think about it for a second.

If the market thinks we’re going to “run it hot” and send asset prices to the moon, obviously we’d get higher inflation. Wealth effects and all of that. Indeed, we saw this play out in 2020-21.

What sort of idiot would lend the government money on a 30-year basis at a reasonable interest rate in this case? They wouldn’t. The bond market would crash. Remember, it’s outside investors that set the marginal prices and yields on bonds, not the Fed.

By contrast, if the market believes the Fed is going to be responsible and enforce sober monetary policy, this will result in lower inflation. You’ll see falling asset prices, lower demand, and less inflation as consumers and businesses prepare for a more balanced macroeconomic environment instead of a series of unending stimulus injections and rolling asset bubbles.

We’ve had a “number only goes up” economy, at least in the U.S., since 2009. Any and all dip buying, in just about any asset, has minted money, while being negative or contrarian has brought only pain. We have a whole generation of professional investors (to saying nothing of recently-minted Robinhood traders) that have never seen a bear market that lasts longer than six months.

Wall Street has been enjoying a raging party for more than a decade.

Many traders want more drugs and alcohol to arrive at our party today -- slash rates to zero, cancel people’s student debts so they can buy more stuff on credit, send out tariff “dividend” checks to folks, etc. etc. Markets were increasingly hopeful that Trump would be able to pick a Fed pushover who would usher in even easier monetary policy and set off another round of mindless “number go up” speculation.

Instead, we got Warsh, a man who was not imbibing at all during the 2000s housing market bender, and who has demonstrated a rather restrained view of the Fed’s need to intervene in the economy throughout his career.

--

So, why did Trump do this?

Occam’s Razor would be that Warsh is a good speaker, he looks good -- “Central casting” according to Trump, and he said the right stuff to Trump to win his confidence. Warsh also married into the Lauder family, who are close to the Trumps.

This is a perfectly logical explanation for why Warsh ultimately got the nod.

But, if you want to look for a more “4D chess” explanation of the pick, here’s my best guess.

If Trump appoints a Fed lapdog that slashes rates to zero immediately, it’d provoke market backlash. Institutional investors (and particularly foreign capital) highly value Fed independence and don’t want to see the Fed run like an emerging market bank. Having Trump set Fed policy via tweet would potentially cause capital flight out of the U.S. and cause bond yields to go up, rather than down.

Warsh potentially solves this problem.

Warsh has bonafide hawkish credentials. The market believes, or at least is open to the idea, that Warsh will maintain sensible level-headed monetary policy, and that -- in particular -- he will be open to raising rates in the future if and when required. In addition, whether you like him or not, Warsh is qualified for the post and already has lots of relevant experience from his previous time on the Fed Board.

The fact that Warsh will be in charge greatly reduces the chance of a runaway inflation/run it hot/plunging dollar train over the next few years. This inherently helps put an upper limit on interest rates, as the odds of a “inflationary rebubble” has dropped significantly compared to a scenario where Trump picked a more dovish person.

If they can thread the needle just right, Trump can get his cake and eat it too; enjoying two or three rate cuts this year while also giving the market a credible hard money guy who isn’t going to let inflation get away from the Fed over the longer-term. In other words, Warsh could put downward pressure on long-term interest rates while also giving Trump his long clamored for headline interest rate cuts ahead of the midterm elections. It’s important to note that Warsh is likely to enforce harder money primarily by slashing the size of the Fed balance sheet rather than clamoring for near-term rate hikes. Warsh can start pushing tighter monetary policy through back channels even while generating the Fed Cuts Interest Rates headline that Trump craves.

Is this balancing act going to work? I doubt it. I think any sign of tighter monetary policy is going to weigh on a market that has been running on fumes. There’s only so far dollar debasement/run it hot narrative + increasingly frenzied AI spending will get you as the labor market continues to weaken.

But, the current Trump economic approach wasn’t resonating with voters. While the stock market keeps going up, only a modest number of voters care greatly about stock prices.

A larger number of folks, including a big chunk of the MAGA base, are not financial whizzes and don’t care about Wall Street much. They’re upset because they perceive inflation as still being way too high and the job market as being bad. Record high stock prices won’t change those feelings.

And all the AI CAPEX spending does nothing whatsoever to improve the quality of life for 80% of Americans (probably makes it worse, in fact, if electricity prices go up). Government policy has been all Wall Street, no Main Street for years now.

Tighter monetary policy would bring down interest rates (good for average consumers, especially folks that want to buy or refi houses) and the majority of the pain would fall on rich people and speculators. Given how bad the midterms are looking for Republicans at the moment, a significant reset of economic policy could be the sort of gamble worth running at this point if you’re a Republican strategist. And that’s doubly true if the Supreme Court strikes down tariffs and Trump has to re-center his economic message anyway.

With that in mind, Trump is now serving up a ton of policy approaches that would make average joe voters happy while angering Wall Street, i.e.:

10% cap on credit card interest rates.

Lower prescription drug prices.

No increase in Medicare insurer reimbursements this year.

Putting caps on how much defense contractors can earn and pay in dividends.

Keep in mind also that Trump originally leaned into the “first Crypto president” thing pretty heavily and launched meme tokens such as the Trump and Melania coins. But these fizzled (down 95% and 99% respectively) and other Trump family ventures such as Eric Trump’s World Liberty Financial appear to be off to inauspicious starts. Perhaps Trump has deduced that he’s gotten all the juice he’s going to get out of closely associating with the crypto and tech bros and it’s time to reorient back toward mainstream Americans where far more of the Republican voter base is.

In that case, the Warsh pick makes a lot more sense, as Trump focuses more on affordability and taking on big business rather than trying to get the price of crypto and the S&P 500 to reach new heights.

--

On gold and silver, as long-time readers know, I own a small amount of physical metals which I bought 10-15 years ago. These represent a mid-single digit portion of my net worth. And I shorted some gold miners equities against them recently as a hedge, as that’s easier than pulling my physical out of storage and finding a dealer that’d give me a fair price.

Why use miners as a hedge here? Since the inception of the GDX ETF, gold miners have delivered barely a quarter of the return of just owning the metal itself:

Mining management teams are notoriously bad. They are, on average, perhaps only better in aggregate than the management teams of small-cap oil & gas names. In other words, the bottom-tier dreck in terms of public company management quality. There are a few good mining CEOs out there, and the world is better for their efforts, but in aggregate, this is a sector where capital goes to die.

I’m content to sit on my modest physical metals position as a hedge against whatever may go wrong in the world (though I’d admit to being tempted to sell if silver stays up over $125/oz long enough to actually get exit liquidity at that price). I hardly ever think about it, it’s a long-term investment that should generally keep pace with or slightly exceed the inflation rate over time. Sometimes, like 2025, it wildly outperforms, but most of the time, it just sits there and doesn’t do much of anything. And on the flip side, ideally I’d close my mining shorts around $4,000/oz gold and $50/oz silver if/when they get back there.

If I had to guess, the run in silver (and the other high-value industrial metals like platinum and palladium) is over. There’s not too much institutional, central bank, or collectibles demand for the less popular high-priced metals -- they ramped up with gold but they’re far thinner/less liquid markets. Silver has some investment appeal, but a large chunk of the market there is still industrial for electronics, soldering, solar panels, etc. And, the higher the price goes, the more it eats away at underlying industrial demand.

This is in contrast to gold, which does act like a Veblen good; that is to say something where demand can go up as the prices goes up. Luxury things like handbags are the classic example where demand goes up as the pricing becomes more exclusive -- arguably the same underlying mechanism applies to gold, at least to a certain point.

In any case, gold is a far more liquid, trusted, and widely-distributed asset than silver, palladium, or platinum. Many people had suggested that gold was a “barbarous relic” and that we’d move on to other stuff like Bitcoins or whatever for our collectible that we could hoard to store value.

However, now that gold has skyrocketed, a lot of people that never gave gold a second thought are starting to view it as a legitimate asset class again. Previously, the stereotype was that gold was for boomers and Austrian economists, but the recent price run has made younger people view gold more positively.

Long story short, the move in silver in particular was so wild and meme-y that I’d guess that last week was the top for it over the next 3+ years. And I doubt other stuff like platinum or palladium is going to new all-time highs again in the near future either.

The exception here could be gold; it didn’t move all that far in the grand scheme of things; I wouldn’t be shocked if gold gets to something like $7,500/oz over the next few years. I’m not predicting it, but if any one of the PMs does shrug off last week’s crash and continues its bull market, gold is most likely. (And copper, while not an expensive metal, is worthy of some discussion which we’ll hit in part two as I think that one can still go higher from here as well)

Don’t I have FOMO that metals prices could go to the moon? No, not really.

It’s tough to own physical metals because they have no yield. A 100oz bar of silver sitting in a bank vault produces no yield, no carry, no dividends, no interest. The price of silver and gold will fluctuate, but over a very long time horizon, it’s largely going to track CPI, which is fine but not great.

And, with some rare exceptions (like the gold royalty companies which I have owned and reco’d here in the past) mining companies produce lower ROICs than their cost of capital -- i.e. they destroy rather than generate shareholder value in aggregate as an asset class. I’m not going to put a ton of money into an asset that either has no yield (physical metals) or which generates negative IRRs as compared to just holding T-Bills.

To reiterate, I do own a bit of physical metals. And I have a higher opinion of the asset class than crypto. People hated that I was skeptical of crypto when it was in its mania phase, and I’m sure some people be annoyed that I think silver has topped now.

It’s nothing personal; I’m an economist by training and have respect for the Austrian/libertarian thinkers. But when an asset turns into a meme, the dynamics change. You can go on about fundamentals all day long but when the price of something triples in a short period of time, there’s a good chance it’s going to sink like a stone once the meme traders start trying to exit.

Silver “Gamestopped” on the way up and you get an inevitable hard correction once the squeeze mechanics exhaust themselves; happens with all exponential rallies, regardless of the underlying thing that has been memed.

Silver will recover eventually, it is far more useful than, say, Dogecoin or AMC’s cinemas, at the end of the day. But in the short run, once you’ve become a plaything for the WallStreetBets crowd, you are going to be in for heavy selling once they move on to a different meme du jour.

To be clear, traders can make money playing these sorts of squeezes and euphoric moves. More than one way to skin a cat in the financial markets. I’m a long-term investor and my focus is in on buying cash-flow generating assets at attractive prices. As such, I don’t spend all that much time thinking about metals, crypto, collectibles, etc. But other people have other preferences, and that’s perfectly fine.

---

But Ian, aren’t you worried about budget deficits/declining dollar/runaway entitlement spending/etc.?

Yes, I am! Fortunately, I have plenty of investment assets which will perform exceedingly well in an inflationary scenario, in particular Latin American stocks.

It’s no coincidence that Latin American markets like Mexico, Colombia, Chile, and Brazil were the world’s hottest equities in 2025 as metals blasted off. LatAm stocks are a way to get substantial upside from commodities/inflation/pro-cyclical activity while having positive yields/carry. In the case of some of our holdings, like the LatAm airports and banks, very high dividend yields in fact, while enjoying plenty of share price gains as well.

This leads to a good question: If in fact the U.S. Dollar has bottomed and metals are topping, is that going to have a big negative impact on our Latin American holdings in 2026? Stay tuned for Part 2...