Rotoplas: A Mexican Industrial Giant In The Making

Water infrastructure leader to rise thanks to skyrocketing margins, 15% topline growth, and great Mexican economic outlook.

Rotoplas (Mexico-AGUA) (OTCPK:GRPRF) is one of the largest water equipment companies in the Americas. The firm was founded in Mexico and at first dealt with storage products such as water tanks.

Over time, it has expanded into many international markets, and acquired or developed a vast array of other water products and services such as filtration units, piping, valves, pumps, irrigation systems, wastewater treatment and so on:

I'm excited about Rotoplas right now for several reasons. For one, it's an industrial Mexican company and I'm bullish on that category in general; manufacturing in Mexico has all sorts of tailwinds at the moment.

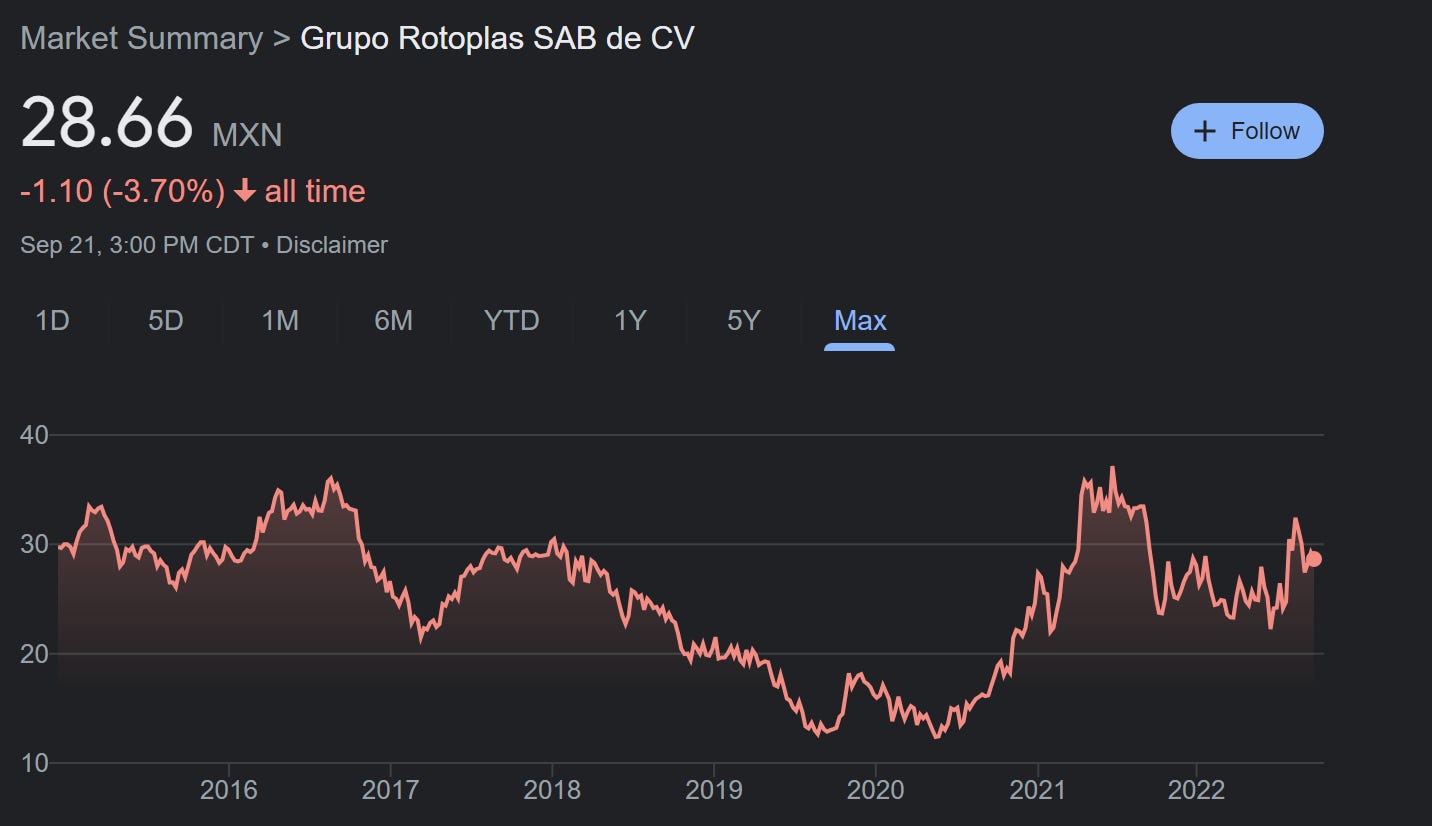

For another, the company has engaged in a massive self-improvement program. It brought in new management and has enjoyed skyrocketing profit margins and operational efficiency since 2019. The stock hasn’t caught up… yet:

AGUA stock surged in 2021, hitting a new all-time high. However, for whatever reason, shares retreated sharply in late 2021, and are now back tobtheir initial IPO price from way back in 2014. Despite the flat stock performance, the company's revenues and earnings power are up substantially since then. I believe the market hasn't appreciated the scope and magnitude of Rotoplas' self-improvement program. As earnings surge in 2022 and 2023, shares could rapidly move to the upside -- I see shares potentially tripling over the next 2-3 years.

---

To get into the Rotoplas story, it's worth investigating the company's business trends more closely and put its recent self-improvement efforts in context. Why hasn't the stock worked historically and what is changing now? Here's Rotoplas' revenues and EBITDA over the years:

One notable thing is that Rotoplas' revenues actually dropped about 15% between 2014 and 2016. This is rather interesting, given that its revenues increased in a reliable manner in all other time periods, including during the Great Financial Crisis. Why was Rotoplas able to grow its business in 2009 but not 2015?

Mexico's Housing Market: The Mid-2010s Crash & Coming Recovery

This is due to the housing market, and the Mexican housing market in particular. Rotoplas currently generates about 50% of its revenues and 60% of its EBITDA from Mexico; this is an international business, but with a solid home bias. That was even more the case back in 2015, prior to Rotoplas' push into the United States market.

So what happened in 2015? That was not long after when the Mexican government suddenly pulled all its subsidies for suburban single-family homes and instead began subsidizing urban apartments for low-income Mexicans. In doing so, this changed Mexico's development pattern totally.

As I laid out in my article on homebuilder Consorcio Ara, this absolutely crushed the Mexican homebuilders. They had bought up tens of thousands of acres of land far outside cities such as Cancun, Guadalajara, and Monterrey, and ended up owning substantially devalued land once the government stopped fronting money for new homes in these far-flung areas.

Homebuilders, not surprisingly, stopped building new homes once it became clear that there was no market demand. Several leading homebuilders went bankrupt, and others that survived essentially went dormant, cutting new supply dramatically as they tried to navigate the new market.

In 2017, however, things came roaring back – at least for Rotoplas. The points the Mexican housing bulls make are correct insofar as there is not enough housing stock to meet Mexico's demographic needs. That's especially true if Mexican families stop having so many generations living under one roof; as the middle class continues to emerge and younger families want to live away from mom and dad, Mexico will need far more housing units.

Builders eventually adapted to changing conditions and started building far more apartments. This was a big shift for homebuilders, but not much of an issue at all for Rotoplas. Whether you live in a suburban house or a 5th-story condo in downtown, you still need a water tank, pipes, sinks, and the like. In some ways, a more urbanized development model should actually favor Rotoplas, since it is working hard to expand its water recycling and treatment operations. A big piece of Rotoplas' ESG push is in reusing water resources locally, rather than trucking in fresh water from far away, which is expensive both in terms of finances and climate burden. Mexico currently relies on a ton of trucked-in water, and that's a big market opportunity for Rotoplas.

In any case, Rotoplas shows the value in being creative when thinking about investments. If you're bullish on Mexican housing for demographic reasons, buying a homebuilder is the obvious first-order thinking solution to the problem. Doing so exposes you to the politics around low-income housing subsidies however, which can be fraught in any country, let alone an emerging market with a strong populist streak.

By contrast, something like Rotoplas which makes all the water equipment for new houses and apartments is much more insulated from regulatory risk. If housing is too expensive, people blame the homebuilder or landlord, few people blame the water tank supplier. And regardless of which economic and urban development model the current crop of politicians favors, it's unlikely that they'll stop prioritizing clean fresh water as a vital piece of infrastructure going forward.

One more interesting angle as it pertains to the housing market. As we've seen in the United States, the pandemic has been a massive driver of new housing demand. People got cooped up in their small apartments or with their parents and said never again. First-time homebuying has soared over the past 18 months.

A similar trend is playing out in Latin American economies, albeit it at a slower rate. Since local governments did much less in terms of providing direct stimulus, cash payments, and extra unemployment to consumers, it took longer for Latin American buyers to shore up their own personal balance sheets. GDP growth, however, did start hitting 10%+ figures in a lot of the region by late 2021 and into mid-2022. Stronger commodity prices, both in Mexico and other Rotoplas markets in South America, should bolster demand for new water infrastructure.

The pieces are in place for an extended economic expansion in Latin America, which would lead to unusually strong activity in the housing market. In the United States, by contrast, housing already boomed and is now entering what could be a significant hangover period. Good for making a year or two of windfall profits if you're a building supply firm, but not something you can plan an extended growth cycle around.

Mexico, by contrast, could enjoy five or more years of strong housing, which would be fantastic news for a firm like Rotoplas.

Rotoplas' Forward Growth

To that point, Rotoplas has guided to at least 15% revenue growth for 2022. That's a baseline number – at least 15%, not an exact estimate. Given that their corporate plan is to double revenues in five years (14% growth rate compounded), 15% for this year is not actually that ambitious. Between higher inflation at the moment and the strong surge in the housing market, Rotoplas should be able to grow the top-line substantially ahead of its longer-term baseline. Last quarter, Rotoplas grew revenues 17% and is ahead of its yearly guidance.

It will be important to keep a close eye on the structure of revenue growth. Rotoplas has a wide array of different revenue streams once you factor in all the countries in which it operates and also its menu of products and services.

These are services such as operating school water fountains and water purification systems for offices and medical centers. As you might expect, profit margin is such higher on the service side of the business, so if Rotoplas is able to drive faster growth there, that will lift the company's overall ROIC and EBITDA margin figures, allowing them to hit their 2025 profitability goals.

Additionally, Rotoplas is targeting 30% revenue growth annually and 45% EBITDA growth annually in the United States through 2025; it believes it owns assets that can be greatly optimized there versus the state in which Rotoplas purchased them from prior owners.

There's an increasingly tried-and-true method of Hispanic owners buying a stagnant asset and repositioning it with marketing and distribution aimed at Spanish-speaking customers. Given the high degree of Mexican laborers that operate in the homebuilding market in the U.S., Rotoplas should have no issues marketing its water tanks and other such products to contractors building homes in fast-growing states such as Texas, Arizona, and Florida.

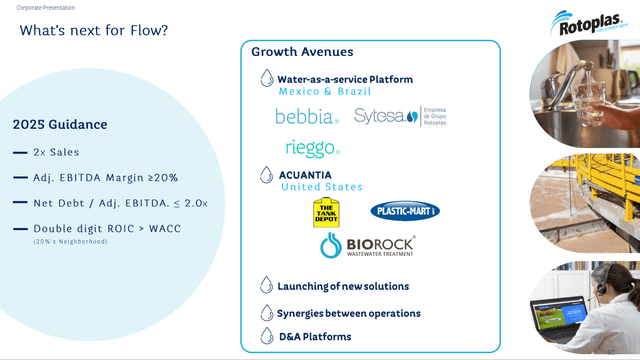

Switching gears a bit, one thing I love about Rotoplas is just how much detail management gives over its five-year plan. They say exactly how much they intend to grow revenues and EBITDA in each market:

And, at the end of the year, they do a checklist of their metrics. In 2021, for example, the company failed to hit its EBITDA metric (it achieved all the others for the year). Management explained that it faced higher costs due to inflation for raw goods, and it chose to take some price to grow its market share rather than reacting with swift steep price hikes.

This sort of numbers-driven model with clear responsibility and accountability if the goal isn't met; it's perfect to see as an investor. For one thing, it's easy to see if the business is on track or not.

Rotoplas Is On A Path To Triple By 2025

If Rotoplas hits its goals, doubling revenues and growing its ROIC to 20% by year-end 2025, we're looking at close to M$3 of EPS annually in that year. The stock price is M$28 now, so that'd be crazy cheap.

In reality, I think a fast-growing ESG-favored water company with an improving margin and growth profile trades closer to 25-30x earnings. That would put the stock at M$75-M$100 in 2025 versus today's M$28 quote. I'm always up for a triple over 36 months.

Can management hit is metrics? The great thing is that we get quarterly updates. The firm is exceedingly transparent with its internal self-improvement program, which it dubs “flow”.

Rotoplas kicked out much of the old management team and have established clear rules and a philosophy for all decisions going forward, centered around the idea that their new investments have to earn double their cost of capital. Over time, this will also boost the company's adjusted EBITDA margin from around 15% to at least 20%.

To date, Rotoplas has approved 470 individual capital allocation decisions in the flow framework, where the company expects to receive a satisfactory return on its incremental capital invested. Employees are incentivized for producing ideas that end up being utilized in the flow program, encouraging everyone to look for bits of waste and inefficiency in the company that can be improved.

Generally, when companies have a strong focus on tangible financial results that directly benefit shareholders – such as improving one's capital allocation – it leads to strong long-term results. I'd argue that's doubly true in a market like Mexico, where many of the country's businesses are not run using any sort of modern consulting or metrics-driven approach.

When Mexico’s Centro Norte Airports (OMAB) explained its recent gigantic special dividend by saying that it would improve the firm’s return on equity, you knew you had something unique. It's just not normal for emerging market firms to view their balance sheets and capital in such a shareholder-friendly way. I think Rotoplas' devotion to improving return on invested capital and rising EBITDA margins will prove to be a similarly fortuitous sign.

Great Upside, Limited Risk

Rotoplas looks particularly compelling when you consider its downside. Prior to the pandemic, the company brought in around M$1.00-M$1.20 per year in earnings. This was before it had begun its drive to improve capital efficiency.

So, even if we write off any benefit from all of the company's self-improvement work, we ignore the rebounding Mexican housing market, and we discount any revenue growth since 2020, we're still looking at a business trading on around 25x pre-Covid earnings. You can assume zero improvement in the business whatsoever and the stock is not aggresively priced today.

There's also not much downside risk in terms of the balance sheet. It has just 1.5x debt/EBITDA. Importantly, all the debt is in the form of a borrower-friendly 2027 ESG bond; in fact, that was the first sustainable green bond issued by a Latin American firm.

This is good news for two reasons. One, you tend to get lower interest rates for debt that can be put into renewable/green investment funds – it's a premium feature in today's marketplace. Two, the company has no debt maturities whatsoever between now and 2027, meaning there is no dilution or refinancing risk anytime soon even if the world economy goes into recession again.

Putting it all together, and the risk/reward here is sensational. On the downside, how far does a dominant water infrastructure and services company really fall? It generally earned at least 1 peso per share per year even when it had subpar capital allocation, so that provides a pretty solid floor for the stock, especially given the strong balance sheet.

On the upside, if management merely achieves their 2025 plan, the stock should triple from here. Shares have been flat since the 2014 IPO even though the business has grown tremendously in size over that span. That was understandable in 2019 when margins had been slipping and people questioned the company's long-term vision.

Several years into the company's self-improvement plan, however, and with rapidly improving operations and returns on capital to show for it, it's long past time that Rotoplas stop trading at a depressed valuation. And, as Rotoplas starts to take off, it will gain momentum.

The stock is still too small to be part of the large-cap Mexican ETF, let alone most international stock funds. I.e. there’s no passive money in this name, yet.

As the company's market cap grows, it will gain more and more entry into ETFs – including those coveted ESG and sustainable funds – further ramping up the momentum behind the stock.

Long story short, I see earnings at least doubling, if not tripling over the next five years. In doing so, the company will attract a lot of fans, powering substantial multiple expansion on top of the earnings growth. Mid-teens earnings growth plus a rising P/E multiple is the holy grail when you're buying an industrial company such as this one. I'm a big fan of Rotoplas at this price and have high expectations for the firm going forward.